We sometimes use affiliate links in our content, when clicking on those we might receive a commission – at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Author: John Ladeluca

Don’t invest unless prepared to lose all the money you invest. This is a high-risk investment, you shouldn’t expect to be protected if something goes wrong.

Forex trading refers to the buying and selling of currencies – with the view of making a profit from ever-changing exchange rates. Crucially, the forex trading industry is one of the largest investment spaces globally – with trillions of dollars worth of currencies changing hands each and every day.

Interested in getting started but not sure how to go about it? Then read our in-depth guide on forex trading. We will cover everything you need to know about such as what forex trading involves, the key trading terms you need to be aware of, how to select a US forex broker, how to trade step-by-step as well as key forex trading tips and strategies to ensure you get off on the right foot!

What is forex trading?

In a nutshell, forex trading is an investment arena that involves buying and selling currencies. Think along the lines of the US dollar (USD), British pound (GBP) and Euro (EUR). The overarching concept is to make money when the exchange rate of a currency ‘pair’ changes price. Each forex pair will have two competing currencies on either side of it.

For example, GBP/USD would mean that you are trading the exchange rate of the British pound and the US dollar. If the current price of the pair was 1.31, this means that you get 1.31 USD per 1 GBP. You would then need to speculate whether you think the price of GBP/USD will go up or down. If you speculate correctly, you make money. If you don’t, you lose money.

How does forex trading work?

Let’s look at a quick example of how a forex trade might work

You want to trade the exchange rate between the Euro and US dollar (EUR/USD)

The price of EUR/USD is currently 1.10

You believe that the value of EUR will increase against USD, so you place a ‘buy’ order.

The value of your trade is $500.

A few hours later, EUR/USD increases by 10% to 1.11.

You close your trade to lock in a profit of $50 (10% of $500).

As you can see from the above example, you placed a ‘buy’ order because you believed the value of EUR would increase against the USD. Crucially, this is always the case if you think that the left-side of the forex pair will increase against the currency on the right. If it does, then the currency pair will increase in value – as it did in the above example.

At the other end of the spectrum, if you felt that the value of USD would in-fact increase against EUR, then you would need to place a ‘sell’ order. This is because you are bullish on the currency listed on the right-hand side of the pair. As such, you would want the exchange rate of the currency pair to go down.

What are the most traded currency pairs on the Forex market?

The trading pairs that have been deemed the largest due to their consistency and large volume in daily trading are as follows (Not in order, as they change the order of most volume obtained daily):

USD/CAD, EUR/USD, GBP/USD, NZD/USD, AUD/USD, USD/JPY, as well as EUR/JPY,EUR/CHF (Swiss Franc), EUR/GBP, and AUD/CAD.

So now that you have a basic idea of what forex trading is, read on to find out how to get started.

Step 1: Select a Forex Trading Platform

Your first port of call will be to select a forex trading platform where you will be able to buy and sell currencies. The best trading platforms come in a range of shapes and sizes, so you need to find a platform that meets your individual requirements. Consider the following factors when joining a new forex trading platform.

How to select a forex trading platform

Regulation : Choose a broker with FCA and CySEC regulations. Ultimately, if the forex trading platform is not regulated, avoid it at all costs.

Payment methods: The supported payment methods will vary broker-to-broker. Ensure you choose a platform which supports your preferred banking method.

Currency pairs supported: Currency pairs are split into three categories – majors, minors, and exotics. If you’ve got a specific pair that you like to trade, make sure that the broker supports it.

Average spreads: Stick with forex trading platforms offering tight-spreads – especially on major pairs.

Trading fees and commissions: In most cases, you will need to pay a commission every time you buy and sell a forex pair. It’s typically expressed as a percentage of the amount you trade. A forex platform with zero-commission trading is preferable.

Leverage: If you’ve got a higher appetite for risk, explore what leverage levels are available at your chosen forex trading platform.

Customer support: It’s best to choose a forex broker that offers customer support on a 24/7 basis. Moreover, go with a broker that offers support via live chat, as this avoids the need to wait for an email reply.

Having analyzed all those features, we have found the best forex trading platform to be Forex.com.

Step 2: Learn these forex terms

Now that you’ve selected your broker, it’s time to brush up on your knowledge of key forex terms. This is crucial, as you need to have a firm understanding of how the investment space works in its entirety prior to depositing funds.

Below we have outlined some of the key terms that you will all-but-certainly come across.

Step 3: Decide on a forex trading strategy

You now need to have a think about the type of trading strategy that you are going to employ. After all, you need to have a clear system in place to ensure you don’t join the 90%-plus majority of traders that lose money.

There is no one-size-fits-all answer as to what strategy you should follow, as no-two traders are the same. However, we have outlined some of the key factors that you should consider when designing your strategy.

Consider your trading time frames

If you like to look at charts daily and want to have several positions open at once, you would be classified as a day trader. On the other hand, if you prefer holding on to your positions for a longer period of time, swing trading will be your strategy.

Define your risk levels

How much are you willing to risk on each trade? Forex trading is a risky form of investment, so consider your losses.

Define your entry and exit points

Determine when you will enter and exit trades. Some people like to enter as soon as all of their indicators give a good signal, while others prefer waiting until the close of the candle.

Use technical indicators

One of the most important tools that you will need to have a firm grasp of is that of technical indicators. For those unaware, technical indicators allow us to gauge the relationship between historical trends and current prices. Depending on the specific technical indicator that you are using, the tool might evaluate pricing movements, volume, liquidity, or a combination of all three.

Popular technical indicators include:

Fibonacci Retracement Levels

Exponential Moving Averages

Bollinger Bands

Parabolic Stop and Reverse

Relative Strength Index

Using technical indicators will allow you to gauge which way the market is going to move next. This is why they should be at the forefront of all forex trading strategies.

Carry out fundamental research

Fundamental research will also inform your trading strategy. This is where you keep an eye on real-world new events that might impact a currency pair. For example, let’s say that you were trading GBP/USD in the weeks leading up to the 2016 Brexit Referendum. It would have been crucial for you to have access to relevant news in real-time to ensure you stayed ahead of the curve.

Regardless of what forex trading strategy you end up using, you need to ensure that you are exposed to important news events as soon as they hit the public domain.

Niche down

With dozens of forex pairs active in the market, it’s virtually impossible for you to have a firm understanding of all of them. Instead, we suggest strongly that you niche down to one or two pairs, with the view of gaining expert knowledge in your chosen currencies. For example, by only trading GBP/USD and EUR/USD, you’ll soon understand what makes the pairs tick.

You’ll also stand a much better chance of predicting which way the markets are going to go, not least because you’ll recognize common patterns. Focusing on a small number of forex pairs will also give you the opportunity to analyze the charts in greater detail, as opposed to trying to evaluate heaps and heaps of different currencies.

Learn about different forex trading tactics

There are a number of trading strategies and tactics that have been proven to work. Some of these include:

Scalping

Bolly Band Bounce Trade

The Bladerunner Trade

The Pop ‘n’ Stop Trade

Forex Overlapping Fibonacci Trade

Daily Fibonacci Pivot Trade

Trading the Forex Fractal

A number of traders active in the online forex trading space engage in these tactics. One of the most popular is scalping, a trading strategy that seeks to make ultra-small profits by holding on to a currency pair for just a few seconds. This can be a highly profitable strategy to employ when a forex pair is in a period on consolidation – meaning that it is trading within a tight range.

For example, if GBP/USD is trading between 1.3110 and 1.3190– and it has done for the past few days, this would be highly conducive for scalping.

We suggest that you read up on all the different forex trading strategies and know them like the back of your hand. This way, you will be able to spot trends and act on them quickly.

Step 4: Open a trade

We are now going to explain the process of opening a trade. We will go through the steps which apply to most forex brokers.

Sign up to a forex broker

The first step will be to sign up to a broker. You will be required to enter your personal information such as first name, last name, username, email, phone number and a strong password. Once done, go through the broker’s verification process and deposit funds into your account.

Select your currency pair and decide whether to buy or sell

Once your account is funded and verified, you will need to decide which currency pair you wish to trade – for example, GBP/USD, EUR/USD, or USD/JPY. Navigate to the search bar and enter your currency pair.

You now need to speculate which way you think the markets will go. To keep things simple – let’s say that you are trading GBP/USD, which is currently priced at 1.29.

Buy Order: If you think that the price of GBP will increase in value against USD, then the exchange rate will need to go up. As such, you would need to place a buy order.

Sell Order:If your more confident on USD increasing against GBP, then the exchange rate will need to go down. As such, you would need to place a sell order.

Set your investment amount

Next, think about how much you want to invest. For example, if you want to purchase $500 worth of GBP/USD, simply enter $500 into the order form.

Decide whether you want to apply leverage

You will also have the option of applying leverage to your trade. If you’re a retail trader based in Europe, then you will need to abide by the limits put in place by ESMA. To clarify, this allows you to apply leverage of up to 25x on major pairs, and 20x on minors and exotics.

Set your stop loss and take profit

Although not mandatory, we would suggest that you at least set up a stop loss order. This will allow you to exit an unsuccessful trade automatically and mitigate your losses.

Finally, we would suggest installing a profit-take order. This operates like a stop-loss order, but in reverse. By this, we mean that you can choose how much profit you wish to make before the trade is automatically closed. If your take profit is hit, you’ll be able to lock in your profits without needing to be sat at your device. Crucially, this allows you to protect your gains regardless of where you are.

Choose a market order or limit order and open your trade

You now need to think about your entry price. If you simply want to take the next available market price, then opt for a ‘market order’. However, if you want to purchase GBP/USD at a specific price, you can do this via a ‘limit order’. In doing so, you stand the chance of entering the market at a more favourable price. When all your parameters have been selected, click on OK and open your trade.

Close your position

If you have set up a stop loss and take profit, the position will close automatically if one of the limits is reached. However, you can also close your trade manually at any time by pressing the red “Close” button. Once your trade is closed, it will be available to view on your history area, and any profits you realized will be available to view in your account balance.

Video summary

We’ve covered the steps to trading forex in the following video summary. The following video will go through the basics of FX trading and how to get started in a simple tutorial.

What types of trading platforms are there?

Forex trading platforms tend to use the “Metatrader” platform, which is a new industry base for integration on the majority of Forex brokers and exchanges. Finding a broker that doesn’t offer Metatrader support in some form or another is a rarity in today’s industry.

Metatrader’s widely renowned platform made its breakthrough with MT4, or Metatrader4. The platform offered a streamlined and global opportunity for all traders to find ease in their currency trading. Then, in an attempt to release an “improved” version of the previously released platform, Metatrader released Metatrader5 (MT5). There are some varied opinions in the overall currency trading community when it comes to which platform reigns dominant. The most important point here: MT4/MT5 are not brokers. They are platforms that can link brokers to enable fast and efficient trading.

MT4

Considered by many as the optimal foreign exchange trading platform, MT4 enables trading through broker linkage. The platform has advanced charting tools that have been tailored for the global currencies market.

MT5

After immense global success with MT4, the Metatrader brand decided to redefine their platform with Metatrader 5 which came with a plethora of new features and capability. This included new complex order types, integration for other markets supported by global brokers including stock trading (including on stock trading apps equities trading, and much more. Overall, MT5 is a bit more complex. MT5 does not allow for hedging forex positions, however, which is a feature that MT4 does allow. Although this is a bit more complex and should traditionally only be derived upon advanced Forex trading knowledge.

But which one should you choose?

MT4 is the more basic option if you’re looking to trade foreign exchange markets. If you’re looking to utilize more complex order types, then MT5 may be the better option for you.

What types of forex accounts are there?

Forex trading is done through a variety of tailored foreign exchange market accounts created specifically for forex traders. The following are the 2 most common types of Forex accounts:

Standard Accounts

These accounts enable you to trade lots in their standard form, which is equivalent to $100,000 per lot.

Mini Accounts

These accounts allow for trading of Forex in what is referred to as lots in their ‘mini’ form; otherwise, denominations of $10,000 per lot.

Understanding forex charts

Understanding charts is very important and can be an extremely useful tool in trading Forex. Prior to learning how to read them and how you can use them to make money trading, you should understand what exactly goes on in a forex market chart.

With this basic understanding, you should have the capability to make very brief and preliminary inferences, such as “This trading pair has been declining in price for over 2 months now”, or “This trading pair dipped down today after increasing for over 3 weeks, maybe now is a good time to trade upward.”

Below, we will outline the most common forex charts and how to read them.

Price charts

The most common chart in Forex trading is the performance of a currency pair over a said period of time. In this case, we can determine the following parameters are used to demonstrate a chart for how the price of a currency pair performs over time. The parameters used in this case are:

The trading pair

The exchange rate (price) of the trading pair

Length of time the exchange rate of the trading pair has been recorded.

In the most standard and most likely used average format of this type of chart, the parameters are used in the following notion; on the Y-Axis, you have a scale that shows the prices that the trading pair has previously obtained. On the X-Axis, you have a start date for where the data recording starts, and then an end date for when the data ends.

A closer look at price charts

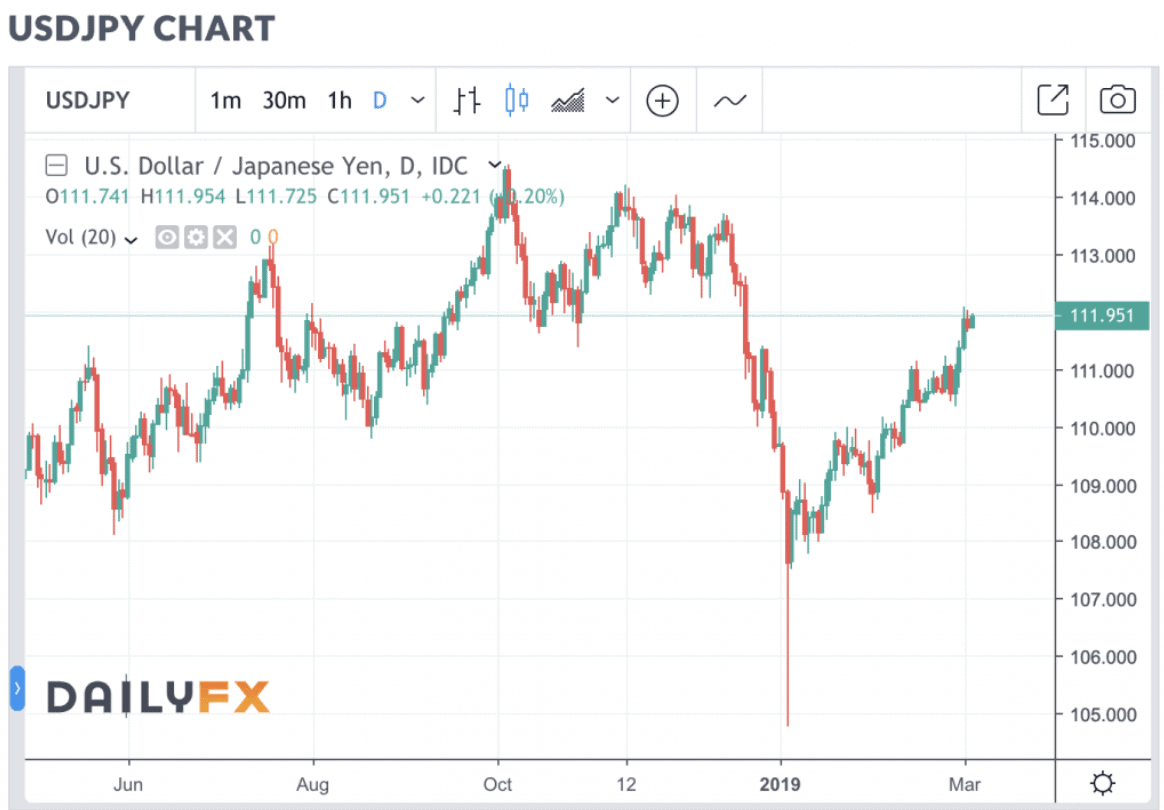

Let’s look at the above chart of USD/JPY courtesy ofDailyFX. At the title of each graph, you will have an overview indication of what it is you’re looking at. In this case, this is the chart for the price of “USD/JPY“. On the X-Axis you can see the time indications, which are marked by Months (Time).

Then as we previously mentioned, on the Y-Axis, we have the price points at which the USD/JPY pair has attained.

Now, let’s delve a bit deeper into the graph. The exact price points may simply look like the prices at which USD/JPY has obtained previously, correct? Yes and no. The above chart is one of the most used and probably most important chart type that you’ll come across, called a Candlestick Chart.

Candlestick charts

A candlestick chart is a type of chart that shows the performance of a currency over time through the form of “candlesticks”. Candlesticks are visual representations of price movements of an underlying currency from its open price, close price, as well as its price increase/decrease relative to the price of the currency on the previous close. This might sound confusing at first, but let’s dive in; candlesticks are a concept that can only be learned with practice.

A candlestick represents a singular time mark relative to the time preference you’ve set. If you are opening a long-term trade then the most popular time frames to visualise your charts with are the 1 day, 1 week and 1 month ones. If you are opening a short-term trade then the most popular time preferences are the 15 minute, 1 hour, 4 hour and 1 day ones. Each candlestick chart will look different depending on what time preference you use. For example if you use the “1 Day” or “Daily” chart a new candle will form every 24 hours, representing 1 Day of price movement.

A closer look at candlestick graphs

Let’s look at a zoomed in version of the USD/JPY chart, which looks like so:

Looking at this chart, each candlestick represents a “Day” of price movement for the USD/JPY pair. Each green candlestick means that on this “Day”, the price of USD/JPY closed higher than what it closed on the day before unless we are talking about the most present candlestick on a candlestick chart. In this case, the candle will be green or red depending on whether or not the price on a “Day” opens relative to the previous day. If it opens higher, then in realtime the candle will appear green.

The following image, provided byInvestopedia, demonstrates the anatomy of a candlestick on a chart.

The topmost part of the candlestick indicates the highest price achieved by the pair during the day; the second topmost is which price the pair opened or closed the day at; the body of the candle extends only as far as the fluctuation in price during the day. The bottom of the body indicates the subsequent open or closing, and then finally, the bottom most part of the candle represents the lowest price attained during the trading period.

Line charts

The second chart that should be understood is the basic line chart. With (Hopefully) newfound knowledge in Candlestick Charts, understanding basic line charts will be easy. Line charts are primarily useful in Forex trading for a preliminary overview of price action. If there are 4 trading screens open across your trading desk, you may not want to know the exact details associated with price action that candlesticks provide. Sometimes you simply want to know the general direction. Basic line graphs are excellent for that purpose.

A closer look at line charts

A line graph displays data in a similar manner as a Candlestick Chart. A basic line graph/chart will overview the price of a certain trading pair over a certain time period. However, it will only ever demonstrate a singular parameter through the chart: which is the close price of the trading pair. Here is the same trading pair we viewed earlier with a candlestick layout, except now replaced with a basic line setup.

Here you can see we have a very broad overview instead of exact closes, opens, and daily movements, and sometimes that’s the only thing you want when looking at a trading pair. This chart is extremely simple in terms of composition: on the Y-Axis, we have the price of the range of prices the trading pair has previously attained, and then on the X-Axis we have our variable of time, which is in months for this specific graph.

Being able to analyze charts is a necessary skill to be able to maneuver any financial market. Learning the functionality and basis of a candlestick chart will be invaluable in your overall trading.

How to make your first forex trade

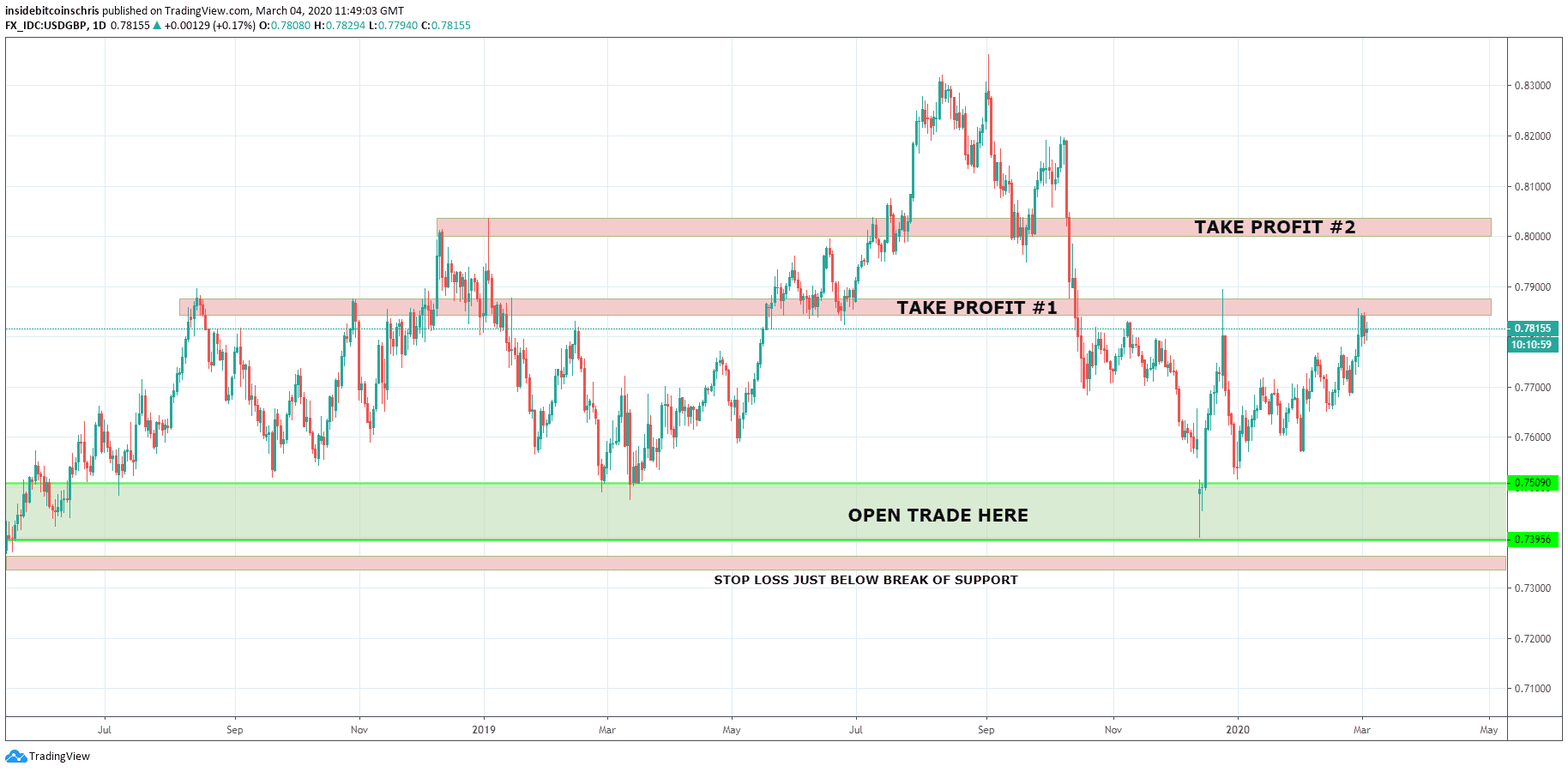

One of the best ways to make your first forex trade is by using support and resistance. Using technical analysis such as support and resistance is a great strategy to ease yourself into forex trading. If you are looking to open a long position (buying a currency with the expectation it will rise in value) then a solid technique is to set your long bids at the support level. Look at the USD/GBP chart below to see how you can set up for your first trade.

1: Find the support level and place long bids there

Support is a price level where there is a lot of demand with many buyers wanting to purchase the currency at that price. In this particular trade set up we can see the support level is from 0.74 to 0.75, so that’s where you should set your long bids. Remember to use a sensible percentage of your portfolio and never risk too much on any one trade.

2: Set your stop loss

The best place to set your stop loss is just below the support level. This is because if support breaks, there may be a steep decline to follow (to the next support), so it’s best to add your stop loss level wherever the support break is.

3: Find your first profit taking point

Before you execute the trade you need to know what level you first want to take profit. The best way of doing this is finding the first resistance level and placing your first profit bid around there.

4: Find your second profit taking point

If your trade is going really well and your currency pair carries on increasing, then you’ll need a second profit taking point. Pick the next resistance and choose that as your second and final profit taking point. Close the trade and enjoy the profits!

Forex trading tips

We would strongly recommend that you read through the tips that we discuss below. In doing so, you’ll stand the best chance possible of avoiding the same mistakes that 90%-plus traders make.

1: Plan your strategy in detail and don’t rush into a trade

Before executing a trade make sure to mark the chart with your entry and exit points. It’s important to note down your desired profit taking point before the trade is executed so your emotions don’t interfere with your trading once it starts. Never FOMO a trade and stick to the plan!

2: Manage risk properly and use stop-losses

Never risk your whole portfolio balance in one trade, calculate how much you want to risk and use a stop-loss to limit risk. A stop-loss order can limit losses and lock in any profits when trading forex. Stop-losses are essential to trading and they trigger even when you aren’t on your computer or phone.

3: Replace demo accounts with small real-world stakes

A lot of online forex courses will advise you to open a demo account when you first get started. This allows you to trade forex without risking your own money. Although this allows you to get a feel for how forex trading works in practice, it’s missing one key ingredient – emotions. By this, we mean that you will never get an understanding of how it feels to lose money when using a demo account.

This is one of the most important battles when trading online, as the emotional side of losing money can often lead to irrationality. As such, we would recommend using a real-money trading account, albeit, with ultra-small amounts. When you then get more comfortable with your trading endeavours, you can up the stakes accordingly.

4: Dedicate sufficient time to forex trading

If you’re thinking about doing a bit of forex trading when you get some spare time here and there, forget about it. The only way that you are going to be successful in this space if you dedicate sufficient time. For example, you’re going to need to spend hours-on-end reading and analyzing various charts, and then trade your findings manually.

You also need to be ready to pounce on a potential trading opportunity if and when it arises. This might be on the back of a technical indicator or signal service. Ultimately, you need to put everything into learning forex trading.

5: Avoid Leverage as a Newbie

As tempting as leverage might be, we would suggest avoiding it in its entirety until you are confident in your abilities as a forex trader. The key problem that you will find is that one unsuccessful leverage trade could wipe out your entire balance. For example, let’s say that you traded EUR/USD at leverage of 25x. Although you only have $300 in your brokerage account, this allows you to trade with $7,500.

However, at leverage of 25x, your trade only needs to go against you by 4% (1/25=0.04) for the order to be liquidated by the broker. This means that you would lose your entire $300 stake. On the contrary, your losses will be minimal when trading without leverage – especially if opting for less-volatile major pairs.

6: Stick With Major Forex Pairs at First

If you’re still a newbie in the world of online forex trading, we would suggest sticking with major pairs at first. This is because the majors are much less volatile in comparison to minors and exotics. Moreover, major pairs also come with the lowest spreads, so your initial fees are going to be kept to a minimum.

This is in stark contrast to exotic pairs, which are highly volatile. Exotics also come with huge spreads, so you would be required to make much larger gains just to get to the break-even point.

7: Take notes and start your own trading journal

There is always something to learn from a trade, whether you make a loss or a profit. During and after each trade make a note of what worked for you and what didn’t. You can learn from your mistakes and always make your next trade even better!

8 : Follow global events

The foreign exchange market is relatively correlated to global occurrences. If the American economy goes into recession, history has shown that typically this means the value of the US Dollar decreases relative to other countries that are stronger. Stay up to date on global developments as this can help the accuracy and profitability of your positions.

9 : Find a strategy that works for you and stick with it

Successful traders become successful arguably because they find something they’re good with and dial in on it. Test out different methods and see which one fits your style the best in terms of risk, and so on. While adopting and learning is never a bad thing, jumping from one concept to the next might not be the best idea as it would yield more profit by being an absolute expert on USD/JPY than being just a mediocre trader on 10 different trading pairs.

Did You Know? If you only want to trade forex part-time, it might be worth using a signal service. This will allow you to receive trading suggestions in real-time without needing to manually read charts.

Is it possible to money trading Forex?

When trading Forex, you are purchasing one currency while at the same time selling another currency. It is possible to make money by either :

Buying a position that increases in value and then selling that position for a profit

Sell a position on a trading pair that decreases in value (similar to short selling) and then purchasing that position back after it has decreased.

While it’s possible to make money, you should remember that most traders end up losing money when trading forex.

Let’s illustrate this with an example:

You open a Forex trading account with $1000 in it. You buy $500 worth of the trading pair AUD/USD at .71 AUD.

Let’s assume margin is not enabled, and let’s also say the price of AUD/USD increased to .72 which is equivalent to an increase of 1.4%. The next day you see this increase and you sell your $500 worth of the position; your $500 has increased by 1.4% (not taking into account fees) which is approximately $507 total. This leaves you with a $7 profit.

The difficult part and the sections that take dedication and time to master are determining the position size to take in your account when to cut losses, when to take profit, and so on.

Which positions should I take in order to turn a profit on my portfolio?

To make profit trading Forex, you look at that question with a very subjective perspective. There is no singular secret sauce that can prove profit in Forex trading, especially with the market at this large of magnitude.

The market is a zero-sum game: when someone loses money, someone makes money and vice versa. Dedication and a sincere amount of diligence and work can return a profitable environment for Forex trading, however, and can increase the frequency at which you place profitable positions.

Learn More: Forex Trading Course & Books

Looking to build your knowledge of forex trading even further? If so, the internet is jam-packed with free information that is likely to be highly beneficial for your long-term forex goals.

With that said, it might be worth checking out other materials on forex – such as an online trading course and books.

Learn2Trade [Best Signals]

Learn2Trade is a UK forex brokers, education hub and signal service. Regarding the former, this includes hundreds of free-to-read guides on everything forex-related. And the latter – Learn2Trade recently launched a forex signals service. Paid members get real-time forex signals straight to their mobile phone or email account, alongside the relevant entry and exit points.

Day Trading and Swing Trading the Currency Markets by Kathy Lien [Best Book] If you’re looking to read a book on the fundamentals of forex trading – look no further than Day Trading and Swing Trading the Currency Markets by Kathy Lien. The author explains everything that you need to know to succeed in a career trading currencies. The book also covers technical and fundamental analysis, as well as the emotional side of trading.

Platinum Trading Academy [Best Course] If you’re looking for a free online forex course that guides you through the basics, we would suggest checking out the Platinum Trading Academy. On top of its proprietary course, the Platinum Trading Academy offers heaps of forex-related videos and blogs.

Conclusion

By reading our guide from start to finish, you should now have a firm grasp of what forex trading is, how it works, and whether or not it falls in-line with your long-term investing goals. As you now know first-hand, forex trading is a highly complex battleground that most people fail to conquer.

This means that you really need to do your homework on key metrics like technical analysis, fundamental research, forex terms, and building your own trading strategy. Ultimately, just make sure that you have a good understanding of the risks of trading forex online before parting with your money, and be sure to choose a reputable, regulated broker with affordable fees and a good range of educational resources such as the platform below.

FAQs

Can you get rich trading Forex?

Theoretically, trading forex can make individuals rich; however, this is no easy task. It requires a large amount of due diligence and research to actually get rich off of the foreign exchange markets. Anyone or any project claiming to be able to get you rich immediately should be avoided or researched.

What is the best way to trade forex?

There are a variety of ways that you can trade foreign exchange currencies. One of the primary ways is by utilizing CFDs, which are contracts for difference; these are contracts which are representations of currency exchange pairs. Additionally, you can simply explicitly trade currency pairs with larger margin imposed.

What is the best forex pair to trade?

There is no singular pair that is the best to trade over any other one. The most liquid trading pairs are as mentioned earlier in the article, which means that you'll be able to execute trades with that pair faster and more efficiently.

Is forex trading legal in the U.S.?

Forex trading is very much available to do in the United States. You can use exchanges/brokers such as OANDA or Ameritrade to kickstart the process.

Is forex trading representative of country economy?

FX markets are to an extent, yes, relevant to an economy's overall performance. If the Japanese economy starts to perform better than the United States, the value of the Yen will in theory increase relative to the US Dollar. This generally is indicative only on a very large scale. This traditionally means that foreign currencies' value is relative to increases/decreases to their economic weight. If the Australian economy were to tank at the same time the US economy were making leaps and bounds, AUD/USD would fall in value.

Is Metatrader able to integrate with all brokers?

Most Forex brokers have enabled Metatrade integration; if they haven't, there is traditionally a third party bridge platform that the broker has worked with to allow integration with Metatrader. Using these bridges can yield seamless adding to Metatrader.

How much do I need to start trading Forex?

You can theoretically start trading Forex with as little as $1 in your account, however, practically, you won't go very far unless you have anywhere from $250 to $500. This will allow you to get a good position in the markets and start a potentially profitable trading account.

John Ladeluca is the founder of the Wall Street hedge fund Banz Capital. He's a blockchain developer, quant, and consultant that specializes in the digital asset sector. He is an authority on blockchain and has written for a number of publications including Forbes.com.

Crypto promotions on this site do not comply with the UK Financial Promotions Regime and is not intended for UK consumers. Note that the content on this site should not be considered investment advice. Investing is speculative. When investing your capital is at risk. This site is not intended for use in jurisdictions in which the trading or investments described are prohibited and should only be used by such persons and in such ways as are legally permitted. Your investment may not qualify for investor protection in your country or state of residence, so please conduct your own due diligence. This website is free for you to use but we may receive commission from the companies we feature on this site.