Join Our Telegram channel to stay up to date on breaking news coverage

- What: The SEC has accused crypto trading platform, Beaxy, and its founder of operating the exchange without a license leading to its shutdown.

- Why: The platform was charged by the SEC for failing to register as a securities exchange.

- What Next: The accused parties resolved to settle without accepting the wrongdoings.

Crypto exchange Beaxy.com has officially shut down after the U.S. Securities and Exchange Commission(SEC) pressed charges against the company along with its founder for failing to register the exchange and running an unlicensed broker, and clearing agency.

The SEC released a press statement stating that Artak Hamazaspyan, the founder of Beaxy, and the exchange unlawfully raised $8 million in an unregistered offering of the Beaxy token (BXY). The statement also stated that the SEC accused Hamazaspyan of misappropriating at least $900,000 for personal use, including gambling.

List of parties facing charges

Based on the complaint by the SEC, Nicholas Murphy and Randolph Bay Abbott maintained and provided the Beaxy Platform as a trading platform that enabled the buying and selling of crypto assets that were offered and sold as securities through Windy, which is a company they managed.

As a result, the SEC is accusing them, in addition to Hamazaspyan, of violating securities law by running an unregistered exchange, broker, and clearing agency, despite the platform being termed defunct by the SEC in a different case last year.

Also facing charges is Brian Peterson and his companies, the Braverock entities, for acting as unregistered dealers due to the marketing services they provided to Beaxy.

You will comply with the law, not the other way around

The SEC Chair Gary Gensler said in the statement that

We allege that Beaxy and its affiliates performed the functions of an exchange, broker, clearing agency, and dealer without registering with the Commission and complying with clear, time-tested rules governing those activities.

He also maintained that the securities laws were established to protect investors and make capital formation easier and cheaper all while improving the markets and he, therefore, stated that “This case serves as yet another reminder to crypto intermediaries that their business models must comply and adapt to the law, not the other way around.”

Gurbir S. Grewal, Director of the SEC’s Division of Enforcement, said that exchanges, brokers, and clearing agencies all had different registration requirements adding that

When a crypto intermediary combines all of these functions under one roof—as we allege that Beaxy did—investors are at serious risk. The blurring of functions and the lack of registrations meant that regulations designed to protect investors were not followed or even recognized by Beaxy.

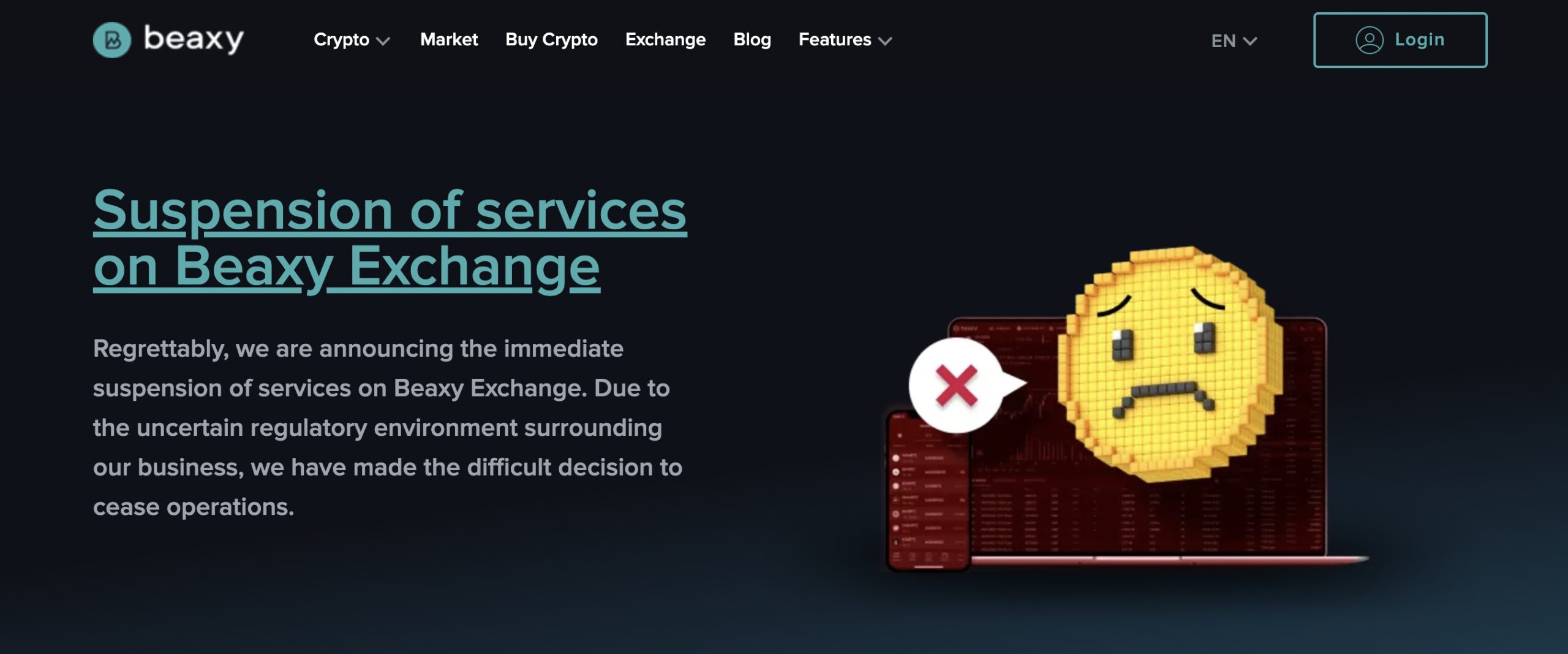

On the hand, Beaxy posted a blog on its website saying that the exchange had suspended its operations citing the uncertain regulatory environment surrounding our business. Beaxy further stated that it had committed to cooperation with the authority for more than two years by providing all the required information, data, and interview.

”Unfortunately, despite our best efforts, it has become clear that the regulatory environment is just too uncertain to continue operations,” the exchange said.

Beaxy assured its customers that their funds are safe and will be made available for withdrawal within 24 hours after all user orders are canceled and balances verified. Customers are encouraged to withdraw their funds within 30 days to avoid any complications or delays, said Beaxy.

More News:

- Why MANA and SAND Holders are Stocking up on Securedverse (SVC)

- Terra’s Luna Price Prediction As $45 Million In Trading Volume Comes In – Can LUNA Swing To $2.4?

- Rogue Nation’s Group Launders Stolen Currency Via Crypto

Join Our Telegram channel to stay up to date on breaking news coverage