In a market that moves like a roller coaster, price stability is a rare comfort. Stablecoins were built to mirror the real-world value of another asset, usually the U.S. dollar, so you can move between positions without going in and out of crypto.

Now, you can use that stability to do more than protect value: You can turn those parked balances into working capital.

In this guide, we explain how to earn interest on stablecoins, where that interest comes from, compare mainstream platforms on convenience, control, and security, and show you how to separate sustainable APYs from short-lived promos.

The Best Way to Earn Stablecoin Interest

One of the easiest starting points for beginners is opening a crypto interest account with a trusted provider, with our top pick being Nexo. It works much like a traditional savings account, but with higher potential yields and instant access to your funds.

Here’s how it works in practice:

- Create a Nexo account: Sign up and verify your identity to get started.

- Deposit stablecoins: Add USDT, USDC, or other supported tokens.

- Hold for the minimum period: Keep your funds in the account to activate earnings.

- Start collecting interest: Interest accrues automatically and is visible in your dashboard.

- Withdraw anytime: Take out your stablecoins and earned interest whenever you’re ready.

Different Methods to Earn Stablecoin Interest

Here are the main methods to earn stablecoin interest:

1. Crypto Savings Accounts

Custodial savings accounts are usually the first stop for anyone testing the waters when trying to earn interest with stablecoins. Simply drop your USDC or USDT into a platform like Nexo or Crypto.com Earn, and the interest starts ticking almost right away.

It is like a regular bank deposit, only your balance is feeding crypto lending desks instead of government bonds. This link to the lending market is what powers the yield. What you earn depends on the fine print. For example, if you lock your coins for longer, hold the platform’s loyalty token, or stick to flexible withdrawals, the APY shifts.

The trade-off feels worth it for many beginners: clean dashboards, daily payouts you can actually see, and the comfort of having support a click away.

Pros:

- Simple setup

- Daily payouts

- No on-chain fees

- Strong UX

Cons:

- Custodial risk

- Rate changes without warning

- KYC or regional limits

2. Stablecoin Staking-Style Programs

Strictly speaking, stablecoins can’t be staked at the protocol level, since they don’t secure networks like proof-of-stake tokens do. However, many wallets and exchanges market “staking” programs that mimic the experience.

In practice, your deposit is lent out or funneled into money markets, but from your perspective, it looks like pressing a “stake” button and watching yields accumulate.

Platforms like Binance Earn and Coinbase Earn wallets offer this style of product, allowing users to stake stablecoins. You usually get flexible withdrawal terms, making it feel less intimidating than fixed-term savings. Transparency can vary, but some providers disclose at least the broad source of returns.

The appeal is convenience, because you don’t need to understand decentralized finance (DeFi), pay on-chain fees, or understand complex mechanics. But the drawback is blurred terminology. Marketing can conflate staking and lending, and users may not always see the actual risk profile behind the APY.

Pros:

- One-click setup

- Flexible access

- APYs often competitive

Cons:

- Confusing terminology

- The yield source may be opaque

- Interest is variable

3. Yield Farming and Liquidity Pools

Stablecoins earn their keep by sitting in liquidity pools. Each swap through that pool generates a fee, and those fees are divided among the liquidity providers, you included. Some protocols also issue bonus tokens to incentivize liquidity providers.

Stable-to-stable pairs, such as USDC/USDT on Curve, are popular because they minimize exposure to impermanent loss.

This reduces exposure to impermanent loss when one token’s value drifts against the other. However, APYs in these pools change constantly based on trading activity and incentive programs.

The upside is higher yields, especially when protocols are pushing incentives. The downside is that it requires active management, so you’ll need to monitor pools, rebalance when emissions fade, and cover transaction fees.

Pros:

- Potentially higher returns

- Reduced price risk in stable-stable pools

Cons:

- Smart contract vulnerabilities

- APY shifts quickly

4. Lending Platforms (CeFi Fixed-Term & DeFi Algorithmic)

Lending is the most direct way to earn yield on stablecoins. On the centralized side, OKX Earn or KuCoin offer fixed-term contracts. You commit funds for a set duration, such as 7 days, 30 days, or longer, and receive a quoted return at maturity.

On the decentralized side, protocols like Aave, Compound, and MakerDAO’s DSR (DAI Savings Rate) allow you to supply stablecoins to algorithmic money markets. Borrowers pay variable interest, and suppliers (that’s you) earn it. You can see utilization ratios and pool metrics in real time, which adds transparency compared to centralized desks.

The appeal here is economic clarity: borrowers pay interest, suppliers collect it. But both models carry risk. In CeFi, you trust the exchange or desk not to default. In DeFi, you trust smart contracts to work flawlessly even in volatile conditions.

Pros:

- Clear logic

- Transparent DeFi dashboards

- Often higher yields

Cons:

- Counterparty risk (CeFi)

- Smart contract risk (DeFi)

- Fluctuating APYs

Best Stablecoin Earning Platforms Reviewed

Next, let’s take a closer look at some of the best stablecoin earning platforms available today.

1. Nexo

Nexo offers one of the most polished stablecoin interest products in the space. Its interest-earning accounts support USDT, USDC, along with other stablecoins, offering both flexible and fixed-term options. Loyalty tiers can further boost yield. Its app is slick, and you can see detailed analytics and AI-driven portfolio insights.

Nexo was launched in 2018, and, after passing regulatory hurdles, began operating in the U.S. in 2024. That opens the doors for U.S. traders to find opportunities to earn up to 16% APY on stablecoins, and they can trust a platform that serves more than 7 million customers and handles more than $11 billion in digital assets.

That 16% APY applies only to 12-month staking plans, but there are also three-month and six-month options at a lower rate.

We rate Nexo for its simple interface, which makes it easy for new users to jump in, its compounding daily interest, and the ability to earn an extra 2% in yield by receiving NEXO tokens instead of the underlying assets.

We also appreciate the easy deposit methods, from debit and credit cards to e-wallets, and 16,000 Trustpilot reviews average out for a score of 4.5/5. 24/7 customer support is also a centralized perk that you will not find on a decentralized platform.

Pros:

- Strong UX and transparency features (dashboards, analytics)

- Supports both flexible and fixed-term deposits

- Loyalty tiers can materially boost APYs

Cons:

- Regulatory issues in the U.S. before 2024

- Rate changes at the platform’s discretion

- Custodial risk (you’re trusting the company’s operations)

2. Best Wallet

Best Wallet is a non-custodial mobile wallet that also enables in-wallet “staking” or yield features by connecting to DeFi protocols and aggregating rates. It supports over 60 blockchains and integrates the Best DEX, which lets users swap tokens while linking into a wide network of decentralized protocols. No KYC is required for basic use.

One of the best features of Best Wallet is the Launchpad, where new crypto projects begin their lives with crypto presales.

During this phase, when the broader market is yet to uncover the latest projects, you can buy presale tokens and then stake them for extraordinary rates, sometimes beating even 100% APY.

For stablecoin staking purposes, Best Wallet pulls together staking opportunities from the dozens of available blockchains and lets you see their APY rates in real-time. This reduces a considerable amount of investigative work and offers you a neutral comparison from across the market, rather than being locked into one provider.

Best Wallet is mobile-first, so you can choose your staking positions on the go and keep everything in your pocket, backed up by multi-factor security and biometrics.

Because it’s non-custodial, your keys never leave your control. The trade-off, however, is that yield opportunities depend on external smart contracts, so you should carry out due diligence on external platforms and protocols. That said, once you are satisfied, you are only a few clicks away from earning yield from decentralized platforms in a no-KYC environment.

Pros:

- Full self-custody (you hold your keys)

- Access to many chains, DEXs, and in-app yield routes

- No KYC for basic use

Cons:

- Yield depends on external DeFi protocols (smart contract vulnerability)

- Less institutional support, limited customer service

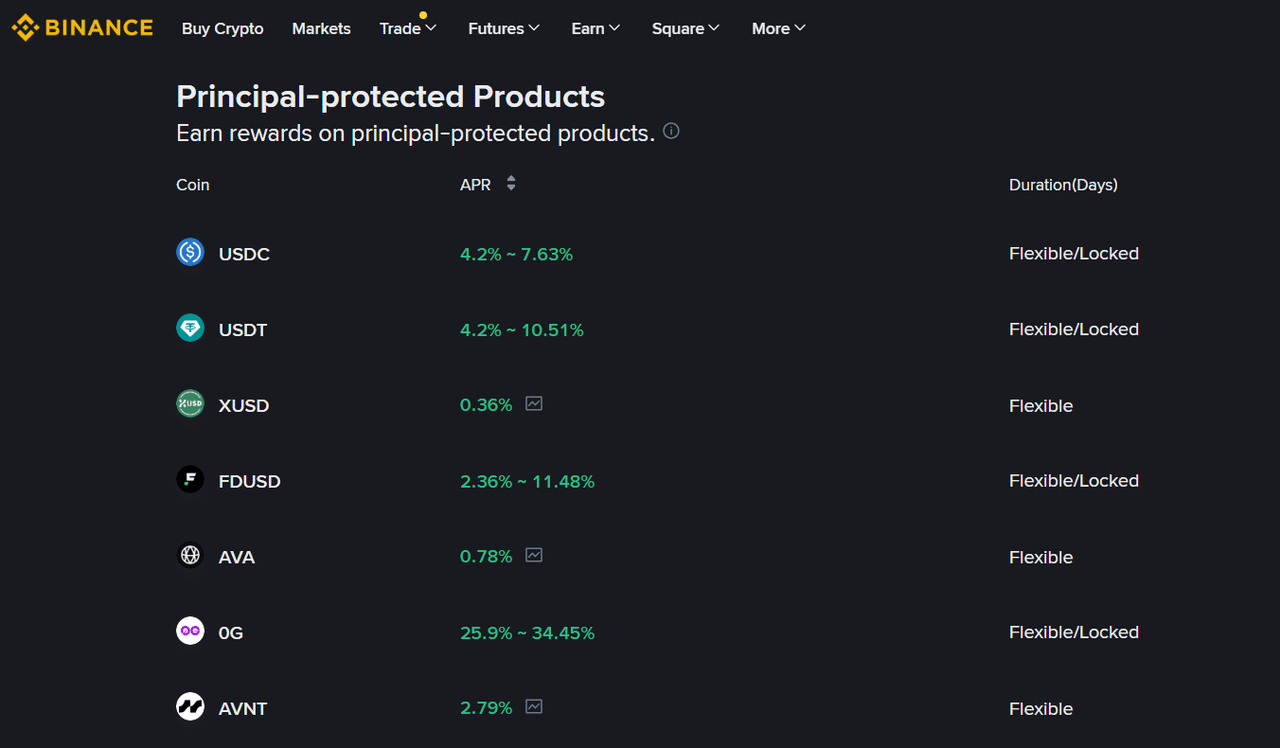

3. Binance (Earn & Savings)

Binance is a giant in the space, and its products let users easily convert stablecoins into yield-earning products. It often combines flexible, locked, and launchpool/incentive programs with hundreds of different ways to choose your own staking adventure.

You will need to explore the options carefully, but we spot staking APYs of between 4% and 11% on USDT, and rates of up to 40% on various stablecoins. You can also yield farm on volatile coins, including Bitcoin.

We note that Binance has a steeper learning curve than other platforms on this list, but the pain may be worth the gain if you are serious about maximizing your passive income. Once you are familiar with the platform, you generally have the option of flexible savings terms or fixed terms (up to 30 days).

Because Binance is mature and well capitalized, it offers reliability and liquidity. But it’s also centralized, so any black swan event (regulatory pressure or a liquidity crunch) could affect users. Also, APYs on highly promoted products tend to drop once new deposit flows slow.

Pros:

- Strong brand, liquidity, and track record

- Variety of yield options (flexible, locked, incentives)

- Integrated ecosystem (trading, staking, loans)

Cons:

- Centralized custody/counterparty risk

- Rate reductions are possible under pressure

- Some restrictions by region/KYC

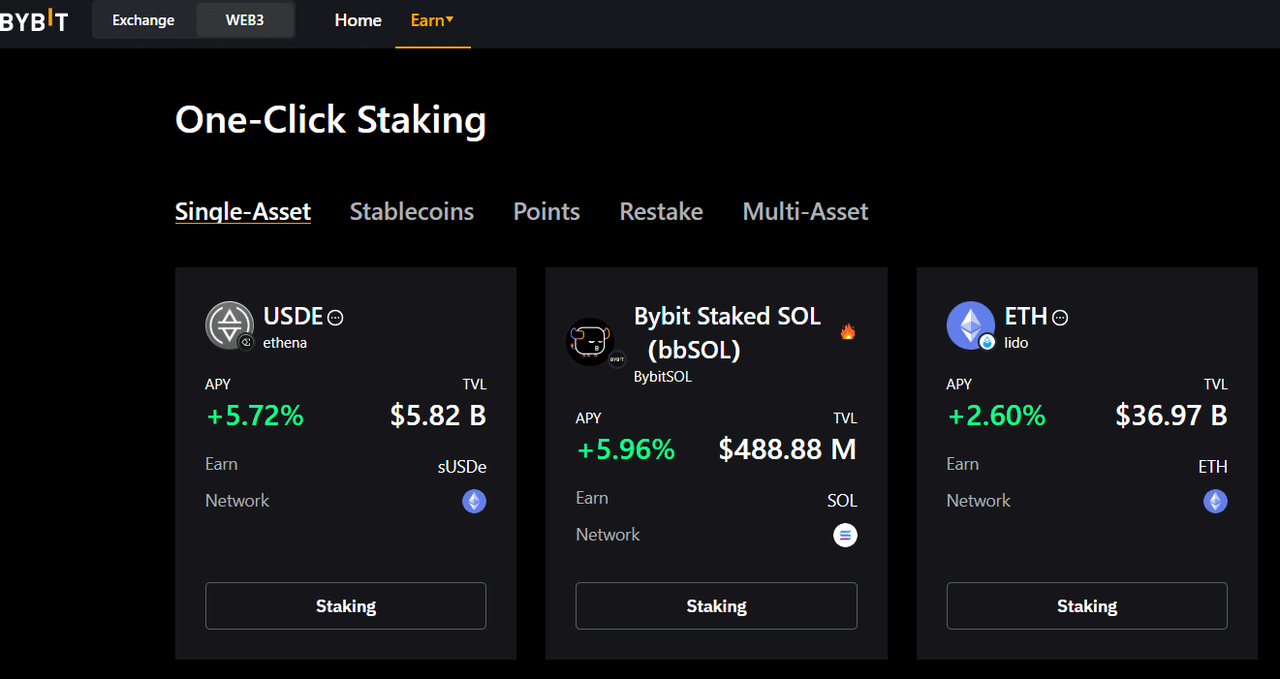

4. Bybit

Bybit is better known for derivatives trading, but it also offers “flexible staking” and “earn” products for stablecoins. For example, USDT flexible staking on Bybit has been praised for offering competitive APRs, especially on smaller balances.

Bybit is a centralized exchange that offers advantages like customer support, but you will need a level of trust in the platform. That said, Bybit has an excellent reputation and more than 70 million users worldwide.

At the time of writing, Bybit offers 7.5% APY on USDT, and above 8% APY on USDC; these are flexible accounts (meaning you can stop staking and remove your funds whenever you wish).

While Bybit is also a platform with a learning curve, we have seen some incredible staking APYs in the high double figures. These come and go, often requiring holding the BIT token to unlock its fullest advantage. However, yield farmers seeking every advantage are likely to find what they need on Bybit.

Pros:

- Flexible staking on stablecoins, decent rates

- Integrated with a robust trading infrastructure

Cons:

- Less transparency around yield sources

- Centralized custody risk

- Regulatory and regional restrictions may bite

How Does Stablecoin Interest Work?

Stablecoin interest exists because markets are always hungry for liquidity. Traders want leverage, protocols need collateral, and exchanges thrive on smooth settlement. Drop your coins into a platform and they’re put to work in those channels, maybe lent through a desk or pooled in DeFi. Either way, the flow generates fees or interest, in turn generating yield that lands back in your account.

The exact mechanics depend on the method. In a custodial account, your provider routes funds into over-collateralized loans or money-market style strategies, then pays you a quoted APY. In DeFi, smart contracts manage pools of digital assets, and borrowers pay variable interest that flows back to suppliers. In liquidity pools, traders pay fees to swap tokens, and those fees are distributed to you as a liquidity provider.

Rates move with supply and demand. When borrowing demand is high or incentives are generous, APYs climb. When demand cools or new liquidity floods in, yields shrink. This is why you’ll see numbers fluctuate across platforms and even from week to week.

Note: You’re not earning “free money” by lending stablecoins. Instead, you’re trading liquidity and safety, whether that means trusting a platform to stay solvent, relying on code to work as intended, or riding out shifts in market demand. The system only makes sense if you understand the source of the yield and accept the risk that comes with it.

Stablecoin Savings Interest vs. Fiat Savings Accounts

Traditional savings accounts at banks feel familiar: you deposit fiat currency, the bank lends it out or invests it, and you earn a fraction of the profits back as interest. In most regions, those rates have been hovering near zero for years. Even now, a “high-yield” savings account might pay 3–5% annually, often with minimum balance rules attached.

Stablecoin savings products work on a similar principle, but they’re plugged into crypto markets instead of government-backed credit systems. Demand for leverage, arbitrage, and liquidity in crypto often pushes rates higher, sometimes into the 5–10% range, and occasionally more during incentive campaigns. This is why they can look more appealing than fiat savings.

The flip side is risk and protection. What banks lack in yield, they make up for in safety nets. In the U.S., the FDIC steps in if a bank folds; in the U.K., the FSCS does the same, covering deposits up to a cap. Stablecoin platforms don’t come with that parachute. If a custodian freezes withdrawals or a protocol gets drained, there’s no insurer waiting to make you whole.

So the comparison boils down to trade-offs: fiat savings accounts give you lower yields but rock-solid protection. Stablecoin accounts offer higher yields and flexibility, but they come with real risks that are sometimes opaque. For many, the solution is to treat stablecoin yields as a higher-risk, higher-return layer on top of traditional savings, rather than a replacement.

How Much Interest Can You Earn on Stablecoins?

The short answer: it depends.

Stablecoin yields don’t follow a single script. One platform might offer just a few percent for flexible deposits, while another dangles double-digit returns if you lock funds or jump into DeFi pools. The spread usually runs from the safer low single digits into the 8–15% range when loyalty perks or promo campaigns kick in.

To give you a feel for the landscape, the table below shows current examples for USDC, USDT, and another major stablecoin across different platforms. Treat them as snapshots; the numbers move with market demand, and they can change fast.

| Stablecoin | Platform | Approx. Rate (APY) |

| USDC | Nexo | Up to 12% |

| USDC | Binance Earn | +7.63% |

| USDT | Bybit | +10.49% (USDT+vSUI earnings) |

| USDT | Binance Earn | +10.5% |

| USDP | Nexo | +8% |

| USDP | Binance Earn | +4.25% |

Stablecoin Interest vs. Non-Stablecoin Crypto Interest

Stablecoin yields usually sit in the middle of the pack. Because they’re pegged to fiat and hold a generally stable value (no price volatility), so lenders and platforms don’t have to offer eye-watering rates to attract deposits. Expect most stablecoin products to hover between 3–10% APY depending on lockups, loyalty tiers, and promotions.

Non-stablecoin cryptos can swing much higher or much lower. ETH, SOL, AVAX will sometimes flash double-digit returns, especially when staking campaigns are hot. But those payouts ride on top of wild price moves and incentive schemes that come and go. You might collect a fat reward one month and watch it shrink the next, all while the token itself lurches up or down in value.

So, the difference is simple: stablecoins offer steadier returns without the wild swings of token prices, making them closer to a “crypto savings account.” Non-stablecoin yields can be flashier, but they blur the line between income and speculation. In other words, you might be earning 15% while your asset falls 30%.

Risks to Consider When Earning Interest on Stablecoins

The first and most obvious is custodial risk. When you hand coins to a centralized platform, you’re trusting their books, their counterparties, and their security. If they mismanage funds or freeze withdrawals, your assets are on the line.

Next, and equally as important, is smart contract risk. In DeFi, smart contracts replace traditional companies, but bugs and exploits are very real. A single vulnerability in a lending pool or liquidity protocol can drain funds overnight, even if the platform looked solid the day before.

You should also pay attention to rate risk. Yields are rarely fixed; they move with borrowing demand and liquidity flows. That 10% headline APY might shrink to 3% next month, leaving you with far less than expected.

And finally, we have regulatory risk. Some interest-earning products have already been restricted or shut down in certain regions, and new rules can change what’s available overnight.

All in all, stablecoin interest can be attractive, but it isn’t a free lunch. Higher returns almost always mean higher exposure, and the safest path is understanding exactly who – or what – you’re lending to before you commit.

What Are the Top Stablecoins for Interest Earning?

Some stablecoins dominate lending markets and exchange volumes, while others are more niche but still widely supported on interest-earning platforms. At the time of writing, USDC dominates DeFi lending pools, according to DeFiLlama’s reports. As of mid-October 2025, USDC-based pools like Maple, Aave V3, and Markl collectively hold over $7 billion in TVL.

Below, we’ll walk through the most important options, why they matter, and what to expect if you park them for yield.

1. USDC (USD Coin)

USDC has become the “blue chip” of stablecoins. Issued by Circle and governed by the Centre consortium (which also includes Coinbase), it’s pegged 1:1 to the U.S. dollar and backed by audited reserves. This transparency makes it the preferred stablecoin for many institutions and a staple across DeFi protocols.

USDC has become the default stablecoin in both CeFi and DeFi. Open a Nexo account or scroll to Binance Earn, and it’s usually the first option you see. Dive into lending markets on Aave or liquidity pools on Curve, and it’s there too, acting as the backbone of most pairs. Returns aren’t flashy, a few percent on flexible deposits is the norm, but promos and loyalty perks occasionally push it higher.

The appeal of USDC lies in its reliability, characterized by strong backing, a clear regulatory posture, and widespread support. The downside is that, because it’s the “safe” option, its yields can be lower than riskier stablecoins. But for most people starting, it’s the gold standard.

2. USDT (Tether)

Love it or hate it, Tether’s USDT is the most traded stablecoin in the world. It dominates volumes on centralized exchanges, particularly in Asia, and often carries slightly higher yields than USDC because of demand in trading pairs.

On custodial platforms like Binance, USDT usually gets top billing with flexible and locked savings products, often running short-term promotional APYs. Bybit also leans heavily on USDT, offering flexible staking options that integrate with its derivatives ecosystem. In DeFi, USDT is widely used in liquidity pools and lending protocols, where its liquidity helps prop up yields.

Tether’s biggest shadow has always been its reserve assets. Questions about what backs USDT have followed it for years, yet the token continues to process billions in redemptions and remains the most used stablecoin in trading. What you get is unrivaled liquidity and utility, paired with a lingering cloud of doubt over just how solid the backing really is.

3. DAI (MakerDAO)

DAI is the original decentralized stablecoin. Unlike USDC or USDT, it isn’t issued by a company, but rather it’s minted by MakerDAO through over-collateralized loans. Users lock up assets like ETH or staked ETH, and in return, they generate DAI, pegged to the dollar.

That structure makes DAI central to DeFi. Lending protocols, DEX liquidity pools, and yield platforms often integrate DAI as a core option. MakerDAO itself runs the DAI Savings Rate, which lets holders earn interest directly through the protocol. Interest rates there can range from a couple of percent to much higher, depending on governance votes and system parameters.

For yield hunters, DAI offers a taste of decentralization but also higher complexity. Returns can be competitive, especially when protocols incentivize DAI liquidity, but risks include collateral volatility and smart-contract exposure. If you’re comfortable with DeFi, DAI is a strong addition to a stablecoin yield mix.

4. USDP (Pax Dollar)

USDP, Paxos’s dollar-backed stablecoin, doesn’t get the spotlight that USDT or USDC do, but it still holds a place in the yield market. Platforms like Nexo and Binance include it in their savings products, often with rates designed to pull in deposits despite the coin’s smaller footprint.

Because it’s not as widely traded, yields can be slightly less liquid, meaning there are fewer places to deploy USDP across DeFi. But for custodial accounts, especially on Nexo, USDP often gets included in the same rate tiers as the bigger stablecoins. That makes it a solid “alternative” if you want to diversify and earn passive income on stablecoins without straying too far from major providers.

The upside: strong regulatory framework and consistent peg. The downside: smaller ecosystem and fewer DeFi opportunities compared to the majors.

5. TUSD (TrueUSD)

TUSD is a fully collateralized U.S. dollar stablecoin issued by Archblock (formerly TrustToken). It’s one of the older regulated stablecoins, with reserves held in escrow accounts and regularly attested by independent auditors. Its supply has grown over the years, especially after Binance integrated it heavily into its trading pairs and Earn products.

On Binance Earn, TUSD has been featured in both flexible savings and promotional locked offers, sometimes with higher rates than USDC or USDT to attract deposits. This makes it a competitive option for yield hunters who want diversification beyond the “big two.” While it doesn’t match USDT’s liquidity or USDC’s institutional reputation, its presence on Binance gives it strong utility in trading and savings.

The main risk with TUSD is that it’s more centralized than it looks. A single company controls issuance and redemption. For most retail users, though, the combination of regulatory oversight and Binance support makes TUSD a viable stablecoin for interest earning.

Conclusion

Earning interest on stablecoins means putting stability to work without abandoning caution. The same steadiness that makes these assets a safer harbor in volatile markets also makes them a foundation for steady yield.

Yield follows utility, regardless of whether you choose a custodial account like Nexo or move toward decentralized markets on MakerDAO. Every return comes from real demand, borrowing, liquidity, or trading, and understanding this link is what keeps the strategy sustainable.

Stablecoin yields may fluctuate, but the main idea is the same: consistency can compound. And in a market that rewards patience as much as risk, this may be the most valuable lesson stablecoins have to teach.

FAQ

Do stablecoins earn interest?

Yes, if you put them into a platform that offers yield. Stablecoins earn because other people are willing to pay to use them. For example, you put USDC or USDT into a platform that puts the stablecoins to work, sometimes through lending, sometimes through liquidity pools.

How do you earn yield on stablecoins?

You earn yield by letting others borrow or trade against your stablecoins. Platforms pool your funds and pay you interest, either from borrower fees (in lending markets) or trading fees (in liquidity pools).

Can I earn interest on USDC?

Absolutely. USDC is one of the most widely supported stablecoins for savings products. You’ll find it on platforms like Nexo, Binance Earn, and DeFi protocols such as Aave and Compound.

Where can you earn savings yield on USDT?

USDT is one of the easiest stablecoins to put to work. Nexo has become a go-to spot for USDT savers, with both flexible and fixed-term accounts that layer in loyalty perks for higher rates. Binance and Bybit list USDT, too, but Nexo’s mix of a straightforward app and daily payouts makes it the easiest entry point if you just want steady returns without extra hassle.

References

- Top 5 Stablecoins by Market Cap and How to Use Them – Forbes

- Are Stablecoins the Future of Payments? Mizuho Analyst Shares Insights – Wall Street Journal

- Traders Lend Out Cryptocurrencies in Quest for Huge Returns – Financial Times

- Stablecoins – Modernizing Financial Infrastructure – Morgan Stanley

- Some Big US Banks Plan To Launch Stablecoins, Expecting Crypto-Friendly Regulations – Reuters